New Services, Greater Income

More DetailsInfo@reliancecapitalfinancelimited.com

R e l i a n c e C a p i t a l

F i n a n c e L i m i t e d

Info@reliancecapitalfinancelimited.com

New Services, Greater Income

More Details

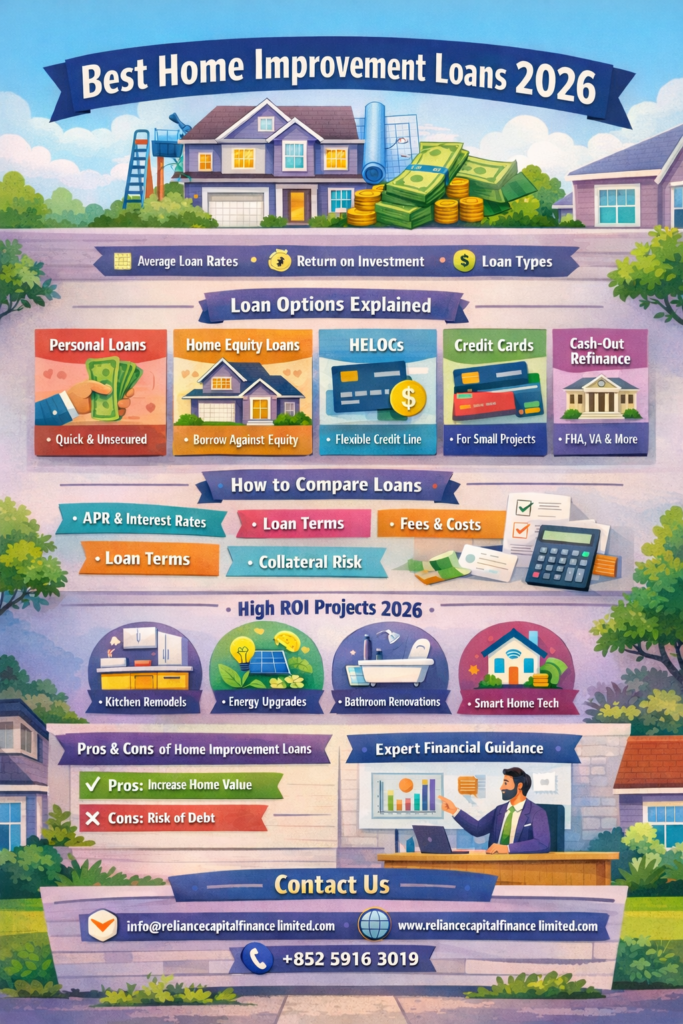

In 2026, homeowners are approaching renovation financing with greater sophistication. Rising property values, fluctuating interest rates, and evolving lending criteria have changed how borrowers evaluate funding options. Therefore, selecting the best home improvement loan is no longer just about securing capital; rather, it involves choosing a structured solution that aligns with your financial capacity, long-term goals, and repayment comfort. Furthermore, it requires structuring debt efficiently, preserving liquidity, and maximizing return on investment (ROI).

Furthermore, this comprehensive guide outlines everything you need to know before financing your next renovation project, including loan types, eligibility requirements, interest considerations, and repayment strategies. It covers average rates, loan structures, comparison strategies, risk analysis, and practical implementation frameworks.

A home improvement loan is a financing facility designed to fund residential property upgrades, repairs, remodeling, or structural enhancements. Unlike purchase mortgages, which primarily focus on acquiring property, these loans are specifically designed for value-adding improvements. Therefore, they can fund projects such as renovations, energy upgrades, or structural enhancements. Furthermore, they support initiatives that enhance long-term property value and overall investment potential.

Home improvement loans generally fall into two categories: secured (backed by home equity) and unsecured (based solely on creditworthiness). While secured loans often offer lower interest rates, on the other hand, unsecured loans rely entirely on creditworthiness. Consequently, your choice determines the repayment structure, collateral requirements, and risk exposure. Understanding these differences allows borrowers worldwide to make informed financial decisions.

Interest rates in 2026 depend on several factors, including loan type, credit profile, and market conditions. Therefore, typical interest rate ranges can be summarized as follows. In addition, borrowers should keep in mind that rates may fluctuate due to broader economic trends and regional market variations. Consequently, staying informed allows for better planning and more strategic borrowing decisions.

Rates are influenced by:

Overall, each financing structure serves a distinct borrower profile and renovation objective. Therefore, to guide your decision-making, the following provides a detailed breakdown that illustrates the differences clearly. Furthermore, understanding these distinctions helps borrowers worldwide choose the option that best aligns with their financial goals.

A personal loan is an unsecured installment loan offered by banks, credit unions, and online lenders. Because it does not require collateral, approval is based primarily on credit score and income stability. Consequently, borrowers with strong credit profiles typically receive more favorable terms.

Key Characteristics:

Best For:

Therefore, this type of loan is best suited for mid-sized renovation projects, particularly in cases where quick approval and a simple process are essential. It provides borrowers with the flexibility to start improvements without unnecessary delays, which means projects can stay on schedule and within budget.

Advantages:

Limitations:

A home equity loan allows homeowners to borrow against the accumulated equity in their property. Since it functions alongside the primary mortgage, it is therefore often referred to as a “second mortgage.” In addition, this type of loan can provide funds for home improvements, debt consolidation, or other significant expenses, which means borrowers can leverage their property to meet financial goals more effectively.

Structure:

Best For:

In particular, it is ideal for large renovation projects, especially in situations where budgets are well-defined and careful planning is essential. Furthermore, because these loans often come with structured repayment terms, borrowers can manage costs effectively while ensuring that the project stays on schedule.

Advantages:

Risks:

In fact, strategic advisory teams—such as those at Reliance Capital Finance Limited—usually recommend performing a detailed property valuation. This step ensures informed decision-making before proceeding with any financing option. Furthermore, accurate valuations help mitigate risk, optimize investment potential, and provide clarity for borrowers in diverse markets.

Essentially, a HELOC provides a line of credit secured against your home equity, which means borrowers can enjoy flexible borrowing and repayment options. Furthermore, because funds can be drawn as needed, it allows homeowners to manage expenses over time while maintaining control of their budget.

Key Features:

Best For:

Therefore, this type of loan is best suited for renovation projects with staggered expenses or budgets that may evolve over time. In particular, it provides borrowers with the flexibility to access funds as needed, which means they can adjust spending according to project phases.

Advantages:

Risks:

Credit cards provide convenience and immediate access to funds, they generally carry higher interest rates compared to alternative financing options. In addition, relying on credit cards for large renovation expenses can increase debt quickly, which means borrowers may face higher costs over time.

When Suitable:

Advantages:

Disadvantages:

Essentially, a cash-out refinance allows homeowners to replace their existing mortgage with a larger loan, and the difference is provided in cash for use as needed. In other words, borrowers can access funds for home improvements, debt consolidation, or other major expenses.

Best For:

Advantages:

Risks:

Consequently, government-supported programs not only reduce the financial risk for borrowers but also enhance access to funding. In addition, these programs often provide favorable terms, which means homeowners and small businesses can undertake projects that might otherwise be difficult to finance.

Examples include:

Benefits:

Limitations:

In particular, contractor financing is provided through renovation companies in collaboration with lenders, thereby allowing homeowners to finance projects directly. Furthermore, this approach often streamlines the approval process, which means homeowners can start renovations more quickly.

Advantages:

Considerations:

Therefore, when assessing financing options, it is important to employ a structured comparison framework so that you can clearly identify the best choice for your needs. Considering factors such as interest rates, repayment terms, and flexibility will help ensure that your decision is both informed and aligned with your financial goals.

Essentially, this metric reflects the total cost of a loan, because it encompasses both interest and any additional fees. Furthermore, by considering all associated costs, borrowers can gain a clearer understanding of their financial obligations. Consequently, they are better equipped to make informed decisions regarding their borrowing.

Opting for a shorter repayment term reduces the total interest cost, but at the same time, it increases the monthly payment amount. In addition, borrowers should carefully evaluate their budget to ensure that higher monthly payments remain manageable.

Because origination fees, closing costs, and penalties increase the total expense, they directly affect overall affordability. Borrowers should carefully review all associated charges so that they can accurately assess the true cost of the loan.

Taking out a secured loan requires caution, because failure to repay can result in foreclosure of your property. In addition, borrowers should carefully evaluate their repayment capacity and consider alternative financing options before committing.

Therefore, when comparing loans, take into account any prepayment penalties, as well as possible refinancing alternatives. In addition, carefully evaluating these factors can help identify the most cost-effective option and avoid unexpected fees.

Running a side-by-side cost simulation for the entire loan term helps borrowers understand total expenses and make informed decisions. In addition, comparing different scenarios can reveal potential savings and highlight the impact of varying interest rates, repayment terms, or fees.

Homeowners should pursue financing only when it clearly enhances either the value of the property or its practical functionality. In particular, this ensures that borrowed funds are used strategically, which means improvements contribute meaningfully to long-term benefits.

High ROI Projects in 2026:

ROI formula:

ROI = (Increase in Property Value – Project Cost) ÷ Project Cost

Strategically, improvements should either:

Proper utilization requires financial discipline.

Avoiding the diversion of funds to non-property expenditures, while maintaining transparent financial practices, ensures that loans contribute effectively to asset appreciation. Consistently monitoring spending and documenting all transactions helps reinforce financial discipline.

Pros:

Cons:

Understanding risk exposure is critical.

Therefore, it is important to borrow only what is necessary, because taking more than needed increases overall interest expenses. Borrowing conservatively helps maintain manageable monthly payments and reduces financial strain.

HELOCs carry the potential for increased costs over time, which means careful planning and ongoing monitoring are essential. Borrowers should evaluate how withdrawals and repayment schedules impact overall interest, so that they can manage expenses effectively.

Homeowners should keep in mind that property values may not always increase as projected. Consequently, it is important to carefully evaluate market trends. Furthermore, doing so helps ensure that financing decisions are both realistic and aligned with long-term goals. In addition, understanding potential risks allows homeowners to plan more effectively and avoid surprises.

Therefore, it is important to plan for potential budget overruns as well as possible delays from contractors when managing renovation projects. Establishing contingency plans and maintaining clear communication with all parties involved can help minimize disruptions.

Borrowers should understand that failure to meet repayment obligations on secured loans may result in the loss of their property through foreclosure. It is crucial to evaluate personal repayment capacity and consider alternative financing options before committing.

Mitigation Strategy:

Because credibility reflects financial reliability, it therefore influences interest rate approval, lender trust, and long-term financial positioning. In addition, maintaining a strong credit profile helps borrowers access more favorable loan terms, which means lower costs and increased negotiating power.

Strong borrowers demonstrate:

Consequently, organizations such as Reliance Capital Finance Limited stress the value of structured financial credibility, because it strengthens a borrower’s negotiating position and facilitates access to more competitive lending terms. In addition, by consistently demonstrating financial responsibility, borrowers can build long-term trust with lenders, which means better rates and improved lending opportunities in the future.

Because creditworthiness affects loan terms, lenders therefore usually require scores of 620+ for secured loans and 680+ for the most favorable personal loan rates. In addition, maintaining a strong credit score helps borrowers qualify for lower interest rates and better repayment conditions.

Therefore, when borrowed funds are used for substantial property enhancements, the associated interest may qualify for tax deductions. In particular, this can reduce the overall cost of financing, which means homeowners can benefit financially while improving their property.

Borrowers seeking the most favorable rates often consider home equity loans or cash-out refinancing options. In particular, these options typically offer lower interest rates and structured repayment terms, which means borrowers can access funds more affordably while maintaining financial stability.

Consequently, hybrid financing strategies are widely adopted for large-scale projects to balance flexibility, cost, and risk. In addition, these strategies allow borrowers to leverage the strengths of multiple financing options. Furthermore, by combining different loan types, businesses can optimize their capital structure while mitigating potential financial exposure.

Personal loans: 1–5 days

Home equity loans: 2–6 weeks

Planning a renovation project in 2026 and require structured financing guidance, then professional advisory support ensures optimal capital allocation and risk management. Furthermore, engaging experts can help you navigate complex financing options efficiently. Consequently, this approach minimizes potential financial pitfalls while maximizing project outcomes.

For tailored home improvement loan solutions, detailed financial structuring, and comparative lending analysis, consider the following key factors. These insights help borrowers make informed decisions that align with both short-term needs and long-term financial goals.

Email: info@reliancecapitalfinancelimited.com

Website: www.reliancecapitalfinancelimited.com

WhatsApp: +852 5916 3019

Best Home Improvement Loans 2026 focuses on strategic financing, disciplined borrowing, and maximizing the economic potential of your property investment. Furthermore, when structured correctly, renovation financing becomes not merely a cost but a wealth-building instrument. Consequently, borrowers can leverage these loans to enhance property value, optimize returns, and achieve long-term financial growth.